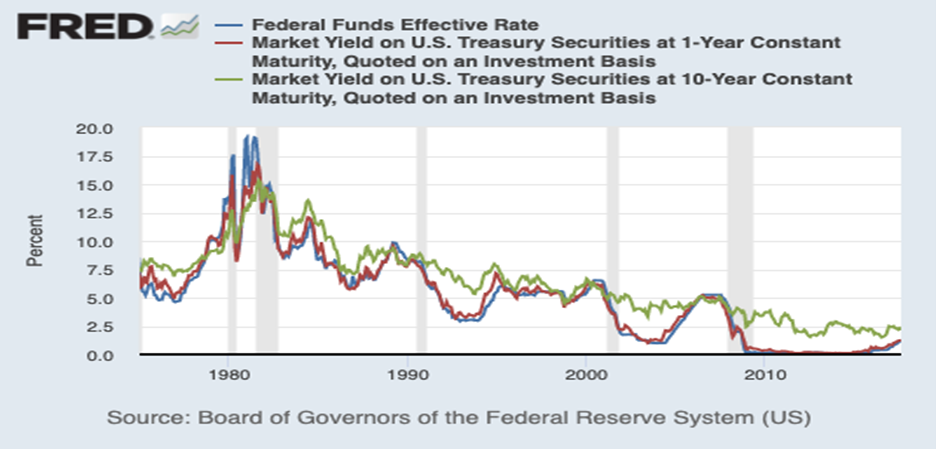

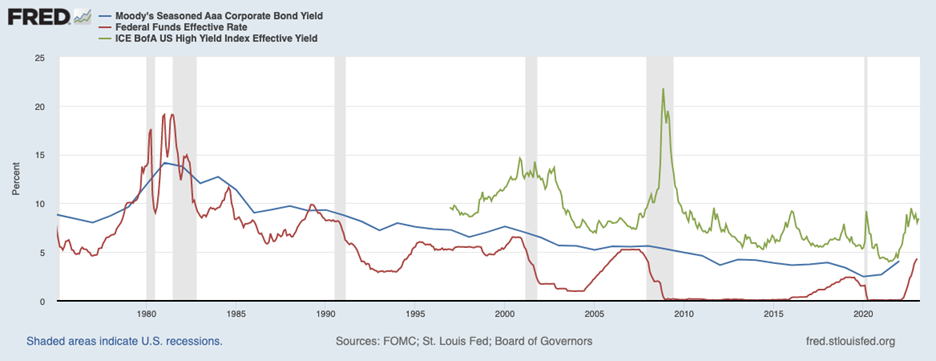

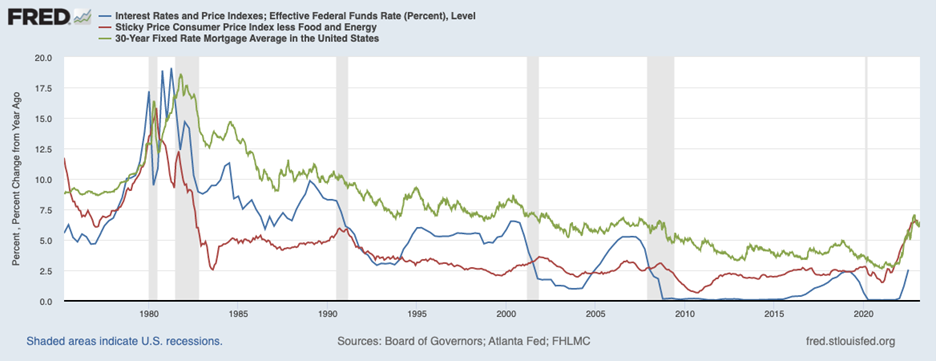

As I dug into the data this morning, I found a few things that were interesting. First, January’s 0.5% acceleration in the CPI was the most since October 2022 (also 0.5%) and you have to go back to June 2022 for a higher monthly acceleration. The general consensus is that higher rates should lead to lower inflation. This means the 2-year inflation expectations in the market should be declining as the Fed gets more aggressive, but as Lisa Abramowicz pointed out this morning, inflation expectations in the market have actually been increasing over the last 6 months. Lisa Abramowicz @lisaabramowicz1 U.S. 2-year inflation expectations have surged over the past six months, despite tighter Fed policy. 1:16 PM ∙ Mar 2, 2023 86 Likes 35 Retweets Inflation expectations are not the only place where the market is being distorted by this central bank intervention though. Charlie Bilello points out that US Treasury yields have gone from historic lows to 16-year highs in...

Comments

Post a Comment